Jul 2nd 2012, 18:21 by R.A. | WASHINGTON

CORRECTION: The perils of the internet age. The motivation for this post was a debate playing out over twitter this morning, between Tyler Cowen, Matt Yglesias, and Matt O'Brien, among others. I grabbed the link to the CFR post mentioned below from this tweet and in my haste to comment neglected to note that it was published in 2010. Mea culpa. Mr Cowen's initial remarks were probably prompted by this new CFR post, which updates the one discussed below. Here are the key charts, updated:

Interestingly, updating the data doesn't much change the story. From the crisis trough in output, Iceland has performed about as well as the Baltic economies and significantly better than Ireland. The key point in the post below stands; the Baltic economies remain substantially poorer than Iceland and most euro-zone members and should therefore be expected to have a much faster rate of underlying growth thanks to the potential for catch-up. That they've essentially kept pace with rich Iceland rather than catching up points to the advantage of adjustment via devaluation, as does Iceland's good performance relative to Ireland.

Put differently, it is telling that to spin a story of growth via internal devaluation one has to resort to citing emerging markets—notably, ones that have managed very little catch up over the past 5-6 years at a time when other key emerging markets were marking enormous gains.

The original post begins here.

PAUL KRUGMAN has spent the past few years making an economic point that used to pass for something like truth: economic adjustments are much, much easier to make when you have a floating currency. It wouldn't have occurred to me a few years ago that it was necessary to defend such an economic point. But apparently it is, and so you have Mr Krugman pointing out that Iceland's economic adjustment, supported by a large depreciation, has occurred quickly while adjustments in the Baltics, where governments have kept their euro pegs, have been protracted and painful. This isn't controversial in the least, but it somehow strikes many writers as both insulting to Baltic governments and people and economically mistaken to acknowledge the data. As I wrote last month:

[T]he macroeconomic facts are not in dispute. Baltic economies are growing once again. But it took a very deep downturn to get them there, including an extraordinary collapse in domestic demand and extraordinarily high unemployment. Despite recent growth, output in the Baltics remains well below pre-crisis levels—below even the trend level suggested by the pre-bubble years before 2005. It is neither an insult to the Baltics or a falsehood to point out that their experience has in fact been remarkably painful.

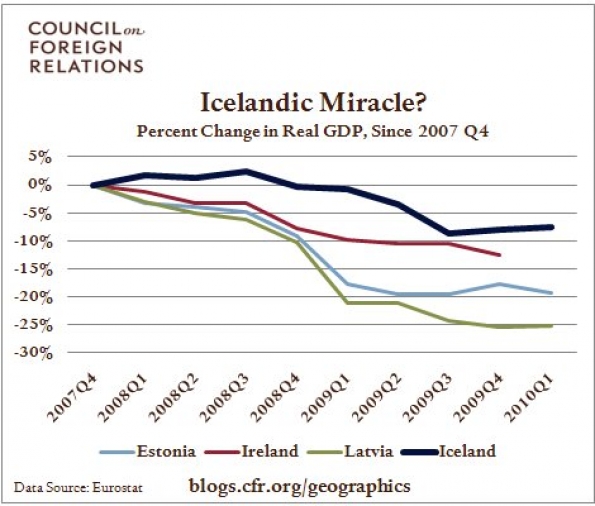

The latest unjustified swipe at Mr Krugman comes from the Council on Foreign Relations. It begins its attack by reproducing a chart used by Mr Krugman:

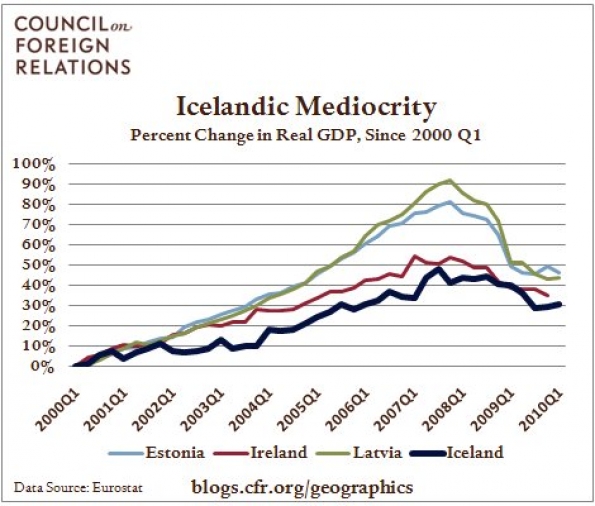

But this apparent good performance, CFR argues, is down to playing with dates. If one zooms out, they suggest, a different picture emerges:

The implication is, first, that Iceland and Ireland have on the whole done worse than Estonia and Latvia, and, second, that to the extent that the Baltic experience has been tough in recent years that's mostly down to the bigger pre-crash boom.

There's a rather significant mistake being made here, which you may well have spotted already: Iceland and Ireland were much, much richer than Latvia and Estonia in 2000. Indeed, if we take a look at per capita GDP, on a PPP basis, we see that in that year Iceland and Ireland were about four times richer than the Baltic states. That is, they were operating close to typical rich-world levels, while the Baltic economies, depressed after decades of Soviet mismanagement, still had lots of room for rapid catch-up growth. Given the scope for catch-up and the boom in the broader European economy, it would have reflected incredibly poorly on Baltic governance if they had not grown much faster than rich Iceland and Ireland. With that fact in mind, the recent performance of the Baltics actually looks far worse. The Baltics ought to be converging with rich-world levels of per capita output. Thanks to the depth of the crash associated with a painful, euro-pegged adjustment, the Baltics spun their wheels in the 2000s, scarcely catching up with advanced economies over the period.

Put differently, unless we assume that pre-crisis growth was mostly bubbly, then underlying Baltic growth is considerably faster than for Western European economies, and the recent growth shortfall has therefore been quite large relative to trend. Either the Baltics weren't heroic reformers prior to the crisis and most of the catch-up from 2000 to 2007 was illusory, or recent Baltic macro policy has been extraordinarily costly.

Now, it's still possible to question the value of devaluation by comparing the Icelandic experience to that in Ireland; Iceland has not done substantially better than Ireland despite the fact that Ireland lacks a currency to depreciate. One is tempted to simply say that these are both tiny, idiosyncratic economies and comparisons aren't informative, but that feels like a cop out. Instead, one could note that exports as a share of the economy are larger for Ireland than Iceland (leveraging any change in competitiveness into a comparatively larger change in the real economy). And one could point out that Ireland's largest trading partners are outside of the euro-area; its biggest export partner by far is America, which has done substantially better than the euro zone over the past year. Iceland's largest export destinations are in the euro area.

Honestly, I'd be happy if we retired Iceland from the macro discussion altogether. It has half the people and one-seventh the real output of the District of Columbia, and fish and fish products account for nearly half of its exports. So long as we're focusing on it, however, its experience relative to the Baltics supports the Krugman view of recovery and adjustment.

Comentários